“The development of our financial oligarchy followed, in this respect, lines with which the history of political despotism has familiarized us: usurpation, proceeding by gradual encroachment rather than by violent acts; subtle and often long-concealed concentration of distinct functions….

……which are beneficial when separately administered, and dangerous only when combined in the same persons. It was by processes such as these that Caesar Augustus became master of Rome.

The makers of our own Constitution had in mind similar dangers to our political liberty when they provided so carefully for theseparation of governmental powers”.

(1914) Other People’s Money and How the Bankers Use It– Chapter I: Our Financial Oligarchy

What you are to read is a collection of stories that have been buried by the captured financial news media. The author takes tremendous risk by posting this online, and it is strongly recommended that you archive this page before it is removed…

As they say, “the golden rule is: he who holds the gold makes all the rules”, and the mega-banks that have seized control over governments worldwide have crowned themselves emperors of our time.

They own the regulators; they own the brokerage houses; they own the clearing houses; they own all of your investments; and it’s even been shown that they can exert complete control over the government.

Over the years, like all despots throughout history, these mega-banks have proven that they can get away with practically whatever they want.

They will print fake shares with absolute impunity, and in effect, artificially control their supply and demand; manipulate corporate elections via their ownership of the shareholder communications infrastructure, influencing who sits on the board of American corporations; and worst of all, they will block anything that threatens their hegemony — even if it can save the elderly 100’s of billions of dollars and revolutionize entire industries.

But why should we be surprised? From the Trail of Tears to the Rape of Nanking; and the Wounded Knee Massacre to the Bataan Death March ; over the ages, history has shown time and time again:

Absolute power corrupts absolutely

The Depository Trust and Clearing Corporation

To understand the essence of their supremacy, one must first understand the securities clearance system. If you happen to be new to all this information, that’s okay — it is very easy to understand.

A clearinghouse is the middleman that sits between a trade, guaranteeing both the buyer and the seller receives their cash or securities. If a buyer or seller fails to deliver the cash or securities, the clearing house guarantees delivery to the counterparties by making up for the loss with their own money.

Without this essential service, a stock exchange will struggle to survive because nobody will be sure if the counterparty will deliver, and all it takes is the slightest bit of doubt for the entire system to collapse. The exchange may be able to operate on a small scale, but not at the capacity that you would expect to see on the NASDAQ or NYSE, and if you have competitors, bankruptcy is not only a possibility, but a certainty.

In the United States of America, there is only one central clearinghouse: The Depository Trust and Clearing Corporation, and for almost 50 years they have maintained a virtual monopoly over this essential service.

It is a private corporation that is owned by these mega-banks and brokers:

Just to give you an idea of the influence these banks have over this institution, we are going to analyze a recent lawsuit filed by a consortium of pension funds against the largest banks and brokers in the United States. It perfectly illustrates their stranglehold over our capital markets, proving beyond any shadow of a doubt that not only will these massive corporations work together behind closed doors to stifle competition, but they also have the ability to instruct the directors of the DTCC to block new entrants that pose a threat to their hegemony.

Before we go any further, it is important for you to understand that there is tremendous risk for those who post this online, and much of what you are about to see has been buried. Don’t be deterred by the length; the article looks much longer than it actually is because of all the screenshots, and everything has been condensed so it should only take you about 60 minutes to read.

If you plan on finishing this later, it is recommended that you archive this page because there is a strong chance that it could suddenly disappear.

A backup bibliography tagged with all the linked keywords is included at the bottom just in case archive.is decides to go under one day.

The links alone took months of research, and many of them are not easily found online. The world of finance is very opaque and litigious, so everybody minces their words and beats around the bush; shrouding simplicity in a long maze of bullshit phraseology and inventive acronyms. There will be none of that in this article — it will be straight to the point. The average millennial — those born between 1981 and 1996 — only has a net worth of $8000, and the gap between the rich and the poor in the United States is almost double that of every other country in the western world. They’ve even started censoring us with Orwellian algorithms that watch and listen to everything we say online. The time for mincing words is over.

But let’s get back to the story.

Stock Loans

There is probably no better example of their anti-competitive behavior than in the stock loan industry, where for the past 20 years, pension funds, endowments, and mutual funds have all been forced to use their services for lack of any viable alternative.

Most of the time, retirement funds tend to hold their investments for very long periods of time, and in order to take advantage of these dormant positions, fund managers will often attempt to increase their clients returns by loaning out these shares to short sellers and market makers so they can be used for arbitrage.

But there is one big problem: still to this day, there is no centralized exchange available for the stock loan industry, which forces massive money managers like Blackrock and CalPERS , along with every hedge fund in America , to employ brokers to match borrowers and lenders, siphoning $100’s of billions from our retirement savings.

Today, most of these transactions are still facilitated over-the-counter, meaning lenders and borrowers have no way of accessing live price data. Only the brokers and “TBTF” banks have access to this information, and this allows them to charge practically whatever they want without anybody knowing if they received a fair market price.

I think the securities lending market is just like the mob. I think it’s completely rigged...It’s a completely manipulated black hole…

–Marc Cohodes, Copper River Partners

The stock loan industry has been described by experts as “the mother of all dark pools“, and people have been calling for change for practically two decades now.

Pictured below is an example of how this process works:

“The current stock loan market involves high search costs and inefficient pricing.

It can take numerous phone calls over several hours to locate a hot stock and negotiate pricing. The lender has no indicative level of pricing other than the demand information provided by the brokers, which the lender has no way to verify. In other words, the securities lending market requires considerable manual effort to complete transactions that in other markets take seconds or minutes at most. Because of the fragmented nature of the market, identical loans can trade simultaneously through different channels at very different prices. These high search costs preclude arbitrage across liquidity pools”

https://archive.is/c0Qt6#selection-24833.5-24875.41

Four companies — Quadriserv/AQS, SL-x, and Data Explorers — all spent several years creating an electronic exchange for this massive $1.75 Trillion market, and their technology could have finally put an end to this backward and opaque system that has been plaguing pensioners, endowments, and hedge funds for more than 20 years. Unfortunately, even though their technology took decades of collaboration and $100’s of millions in start-up capital, they were all blocked by these mega-banks.

It threatened their cartel

The mega-banks that dominate this industry simply had too much to lose by allowing us to have access to this information, so in order to stop this technology from reaching the market, they banded together and refused to provide key services to these bright start ups, even going so far as to threaten their top hedge fund clients with the loss of critical prime brokerage services if they found out they were using their platforms.

In 2016, it was estimated that these brokers were extracting as much as 65% of the revenues from the stock loan market, most of which was going to a very small group of investment banks.

The cumulative effect this can have on our pension funds is astronomical. Just to put that into perspective, Frontline estimated that as little as a 2% annual fee charged by your average mutual fund over a period of 50 years would result in a 66% reduction to your retirement savings.

On an annualized basis, the stock loan industry is said to produce $9 billion in revenue. That equates to $180 billion in profits over a period of 20 years, and this is without accounting for compounding interest. Quadriserv — one of the companies that attempted to challenge these brokers stranglehold over the industry — estimated that their platform could have saved pensioners $4.5 billion per year, and one veteran bank executive was even quoted as saying that it could “do the work of six traders in one ”.

Now, you might find this part hard to believe, but it has also been alleged by reliable sources that for several years these mega-banks and brokers have been conducting “private gatherings” for the purpose of coordinating elaborate schemes so they can maintain their dominance over this essential financial service; what they jokingly refer to as a meeting of the “Five Families” — a mafia related term that they will often use to describe themselves collectively. This should clearly indicate to anybody how little these people probably care about the lives of average hard working people (or even how much they should be trusted for that matter).

Just click on those links and see for yourself. It should take you to the exact line of text. If the link stops working, just highlight the keyword and you can find an excerpt at the bottom of the page.

The New York Clearing Association

As we all know, history has a tendency to repeat itself, and the brazen anti-competitive behavior showcased in that stock loan lawsuit is certainly not the first time something like this has happened. It almost perfectly emulates the Cartel from the days of the New York Association, when a consortium of the country’s largest financial institutions could shutdown any bank in the nation simply by refusing their services. In fact, it was this very behavior that eventually went on to become the primary focal point of the Pujo Committee in 1913, immediately before the passing of the Federal Reserve Act.

Included below are key excerpts from this Committee that will show you the true power of a clearinghouse. Quotes from the book, “Other People’s Money and How the Bankers Use It” (1914), a collection of essays written by Louis Brandeis during that time period, will also be included, and everything has been broken down so it will only take about 5 minutes to read.

From the Depository Trust and Clearing Corporation’s 2018 Annual Report

(February 28, 1913) “Report of the Committee appointed pursuant to House resolutions 429 and 504 to investigate the concentration of control of money and credit”.

Knickerboker Trust was banned from using the clearing services of National Bank of Commerce of New York, leading to its immediate collapse.

Without the services of the the New York Association, the most dominant Clearing House at the time, it was well known by customers and bank owners alike that they would almost certainly fail within as little as a few days.

Even so much as a rumor would cause a bank run

The New York Clearing House forces Oriental Bank to stop working with two Brooklyn Banks, even though they pose no risk to anybody and represent an important percentage of Oriental Bank’s profits.

“The men who through their control over the funds of our railroads and industrial companies are able to direct where such funds shall be kept and thus to create these great reservoirs of the people’s money, are the ones who are in position to tap those reservoirs for the ventures in which they are interested and to prevent their being tapped for purposes of which they do not approve. The latter is quite as important a factor as the former. It is the controlling consideration in its effect on competition in the railroad and industrial world.”

–(1914) Other People’s Money and How the Bankers Use It

A sort of gentleman’s agreement decided the fate of the entire country..

“These bankers are, of course, able men possessed of large fortunes; but the most potent factor in their control of business is not the possession of extraordinary ability or huge wealth. The key to their power is Combination….

“There is the obvious consolidation of banks and trust companies; the less obvious affiliations–through stockholdings, voting trusts and interlocking directorates–of banking institutions which are not legally connected; and the joint transactions, gentlemen’s agreements, and “banking ethics” which eliminate competition among the investment bankers”.

–“Other People’s Money and How the Bankers Use It”, (1914)

All it took was 1/4 of its members to block somebody from joining, regardless of their qualifications, and even if these people were competing with the appellant.

Even if the bank was a member of the club, in the event of a change of control, the bank would be expelled if the members did not approve of the new management. It’s a clique; a private club; a Cartel.

Do you see how powerful these organizations are? They shutdown two healthy banks for no reason whatsoever. People’s life savings were in those banks, and this was before social security, so you could literally starve back then; you and your family.

What most people fail to recognize is that profits are only secondary to these mega-banks. Following the repeal of the Glass-Steagall Banking Act and the massive bailouts that followed, these corporations have becomes empires, and there’s a reason why the blood drained out of that banker’s face at the mere mention of Quadriserv’s technology, but it has very little to do with profit.

It’s about control.

If the stock loan market were to emerge from the shadows of the “OTC” and on to a public exchange where everything is closely scrutinized, it would be much easier to track who was borrowing stock, and at what price, which could potentially reveal what these mega-banks are up to behind the scenes. People might even start recommending that they include all these loans into a Consolidated Tape, making it much harder for them to hide their activities.

“Under Graber, I learned that Wall Street was an illusion,”.. “There were different magicians using different tricks in different ways. But everyone cheated. It shocked me so much in the beginning. I admired these people. And they cheated”.

—Samuel Israel III

Keeping this market in the dark doesn’t just give you control over the spread, like what is seen here:

It gives you control over the supply of equities, and it also allows you manipulate voting outcomes in contested elections.

“And then as time went on and/or a position got bigger, the rate would get jacked up on us…… So our cost of doing business in a particular name would

go from not costing us anything to costing us tens of millions of dollars”…

—Marc Cohodes, Copper River Partners

The same thing happened before the financial crisis when CDO’s were still popular. They refused to allow anybody to access live pricing data, so everything had to be traded on the OTC markets with no centralized clearing. Even when they were offered the opportunity to trade on a public exchange, they still refused, and it would’ve saved them money..

If somebody were to tell you that you do not technically own your shares in a public company, you probably wouldn’t believe them would you? That seems rather ridiculous, doesn’t it? Many people have their life-savings invested in the stock market, and how could somebody else own something that you paid for with your own money?

Unfortunately it’s true, and you are not the legal owner of your investments. The banks and brokers are the true legal owners, and you are just issued an entitlement; an unusual relationship that they characterize as “street name” ownership, and all shares are held in book-entry form (electronically) at the DTCC, with the banks and brokers acting as the registered holders on the company’s books.

By transferring ownership to the DTCC and registering the brokers as the true legal owners of your investments, it solved the problem of constantly having to transfer physical certificates from one location to another; a process that was cumbersome and created liability issues.

Back the in the 70’s, they describe this unusual relationship as a “Jumbo Certificate”

A perfect example of this ownership structure is illustrated in the document snapshot pictured below from a recent Broadridge Financial Services note offering, dated Dec.5th, 2019, only a few months ago.

They refer to this debt obligation as a “Global Note ” that is owned by the DTC (a DTCC subsidiary).

It also says that the owners of the “beneficial interests” will not be legally considered owners of “any notes ” under the “Global Note”. A “beneficial interest” would be you, as you are the brokers’ customer for which they have granted you “entitlements ” to these investments.

“Under Article 8, the beneficial owner of the shares held in a custodial account with an intermediary (such as a broker) is considered to be the holder of a “securities entitlement” in a “financial asset” which is ultimately held by a depository”, —Marcel Kahan, The Georgetown Law Journal

They say explicitly in the first paragraph that the DTC will credit the “beneficial interests ” represented by the “global note ” to the accounts of the “participants“.

But who are these participants?

The “participants” are the same banks and brokers that are buying the debt securities from Broadridge.

But doesn’t that make them the indirect owners of this “Jumbo Certificate ” — or in this case, “Global Note ” — through their ownership of the DTCC?

The answer is yes, it does.

In the age of artificial intelligence, crypto currencies, smart phones and quantum computing, you might be wondering why we still need these brokers and banks to act as the legal owners of our investments. Nobody uses paper certificates anymore, and certainly there should be some kind of SAAS technology out there by now that could solve the liability and book-keeping issues that come with transferring these ownership interests back and forth between accounts.

In reality, this system hasn’t been necessary for practically 20 years, and many experts are equally as perplexed by this unusual “entitlement ” system as they are about the opaque black-hole that governs the stock loan industry today, where retiree’s (“the elderly “) are literally being forced to utilize middlemen that actively collude to separate buyers and sellers so they can charge higher spreads.

They don’t even let companies send “proxy” (voter) materials directly to their shareholders; the company is forced to send the voting materials to the brokers first, and only then will they send them to you.

Pictured below is an illustration of how this process works:

If you had trouble with that first one, this next illustration might be easier to understand. The other one is kind of old — from 1976 to be exact.

Yes, the same system that existed back then is still being used today.

Take a guess who these brokers contract out to send you these “proxy” materials (voting cards).

Broadridge Financial Services..

They control 80% of the “proxy” (voter) communication industry. Don’t worry, we’re just getting started. It gets much worse.

Did you know that you can borrow shares immediately before a corporate election for the sole purpose of influencing the outcome? Yes, in America if you borrow shares, the voting rights will be transferred to you.

You get to keep the dividend, but not the vote? Seems rather counter intuitive, doesn’t it? Or better yet, rife for exploitation?

..That’s because it is..

“The existing system of shareholder voting is crude, imprecise, and fragile. Gil Sparks, a leading Delaware lawyer, estimates that, in a contest that is closer than 55 to 45%, there is no verifiable answer to the question “who won?”“

—The Hanging Chads of Corporate Voting

Over and over again, and for multiple decades, it has been shown that votes are constantly being misappropriated, yet the only entity that can reconcile this problem is owned and controlled by them: The Depository Trust and Clearing Corporation.

Broadridge, the company they contract out to send us our proxy (voting) materials, even admits in their corporate filings that their relationship with these brokers constitutes as a “conflict of interest “.

Should we really trust these people to fairly tabulate our votes? You can make $100’s of million’s from being on the right side of a corporate merger, and as recent history has shown, these banks will rig anything so long as they can get away with it. Only 30% of shareholders were shown to have voted in 2014, and as we all know, there is no better industry than Wall Street at finding legal loopholes, so rigging such an opaque and outdated system should be a piece of cake for these mega-banks.

That alone should be enough cause for concern, but combined with the fact that they can borrow shares for the sole purpose of influencing an election, and it’s easy to see how this system could be manipulated. They even have a name for this practice: Vote Buying

Yes, Vote Buying..

From now on we’re going to try to avoid using the word “Proxy” because it acts to cloak what is actually going on: a vote, not a “proxy”. That word makes it sound much more complicated than it actually is, especially considering all the technology we have today. Every country in the western world holds elections, yet for some strange reason, the only place that exhibits such unusual complications is on the stock market; the lifeblood of the American economy.

Bob Drummond wrote an article about this for Bloomberg years ago, but in typical Bloomberg fashion, it was deleted).

“It is an abomination,” says Thomas Montrone, chief executive officer of Cranford, New Jersey-based Registrar & Transfer Co., which oversees shareholder elections. “A lot of the time we have no idea who’s entitled to vote and who isn’t. It’s nothing short of criminal.”

“In a little-known quirk of Wall Street bookkeeping, with the growth of short sales, which involve the resale of borrowed securities, stocks can be lent repeatedly”.

https://archive.is/PR9Ww#selection-3583.0-3586.0

….”The loans allow three or four owners to cast votes based on holdings of the same shares”.

https://archive.is/PR9Ww#selection-3587.0-3590.0

Drummond later described three specific contested elections where this was known to have occurred. As you can see in the image below, all one needs is a few extra shares to tip the pendulum in a contested election, making the corporate executives and wolf -packs who front-run these predatory schemes millions from carefully facilitated mergers, acquisitions and hostile take overs.

(CARL T. HAGBERG AND ASSOCIATES) “Over-voting is, quite simply, untenable. Allowing it to continue makes a mockery of the idea of corporate democracy. There is ample evidence that people do try to “game” the system, since votes do indeed have value – especially when the voting outcomes have the potential to move the stock price, as often they demonstrably do. (See, for example, “Vote Trading and Information Aggregation” which is easily accessible on the Internet and which documents huge spikes in share purchases near meeting record dates and corresponding sales immediately thereafter). There is also a great deal of evidence that the “gamesters” quite often succeed in gaming the vote, since, (a) as the study pointed out, one can buy votes for about $6 per million votes and (b) vote buyers will vote 100% of the time, while long-term owners tend not to vote at all, which allows the voters with “duplicate voting credentials” not just to go undetected, but to have their way in terms of the election outcomes. It is especially important to note in the context of election “gaming” that the interests of short-term and long-term owners are, almost always, diametrically opposed in election contests”.

https://archive.is/aUv1B http://www.sec.gov/comments/s7-14-10/s71410-68.pdf

“The customer doesn’t know this is happening,” says John Wilcox, head of corporate governance at TIAA-CREF, the biggest private U.S. pension plan for teachers. Often, the broker still permits the customer to vote the shares even though they’re out on loan. That policy is not sound. It definitely means that shares can be voted twice.”

https://archive.is/PR9Ww#selection-4015.0-4018.0

But most of the time none of these tactics are necessary, because again, people usually don’t even show up to vote anyways.

“It’s invisible,” says Paul Schulman, executive managing director of Altman Group Inc., a proxy solicitor based in Lyndhurst, New Jersey. Most of the time you don’t get overvotes because so many shareholders don’t vote.”

They’ve certainly shown that they are perfectly capable of rigging everything else. These companies will do anything to buff up those quarterlies; they will even instruct the directors of the DTCC to block new technology that can save pensioners hundreds of billions of dollars.

Pensioners: those people who worked their whole lives and finally want to settle down after decades of toiling at their job 5, maybe even 6 days a week. They took you to school, fed you while you were a child; taught you everything you know about life..

Think about it this way: not only will these banks steal from the future by printing trillions of dollars so they can cover their reckless stock market bets, but they will also steal from the past by siphoning value from your retirement savings..

None of this is a conspiracy. You can click on the image below and it will take you directly to the exact line of text.

Just imagine the power you would have if you could manipulate the voting outcomes in a corporate election.

Just going off the Wilshire 5000, the combined market cap of every publicly traded company in America is equal to roughly $33 trillion, and some of these corporations are larger than most countries. Directors can also exert significant control over the company finances, and they pour billions into our elections.

“How Broadridge and its customers—the bank and broker custodians—adjust overvotes, revocations, and other problems within its system is entirely opaque”.

—The Hanging Chads of Corporate Voting

If you wanted to influence the outcome of an election, what do you think would be the easiest way to accomplish this? You would probably want to wait until you could see the results first, right?

Guess what, that’s how they can do it! It’s up to them whether they want to count the votes before, or after receiving the tallies. Yes, they can literally wait until they know the results, then tabulate everything knowing what the outcome is going to be.

Just imagine if the American people found out a political election was being handled like that? There would probably be a revolution the very next day..

… “there is no guidance in the rule (NYSE’s Rule 452) itself or from the Exchange in any other form as to how a member firm is to handle a situation where it receives proxy voting instructions for more shares than it holds in record ownership. Thus a member firm apparently enjoys substantial flexibility when it cannot act on all the instructions received, and in particularit presumably may select at its own discretion which voting instructions it will disregard“ . . . (SEC (1991), p. 28)

Vote Trading and Information Aggregation,

This is just the beginning. There is much more.

Let’s say there is a voting discrepancy because these TBTF banks and brokers decided to issue more voting entitlements than actually exist; it turns out that the entity that counts the votes doesn’t even have a fixed procedure for dealing with this problem.

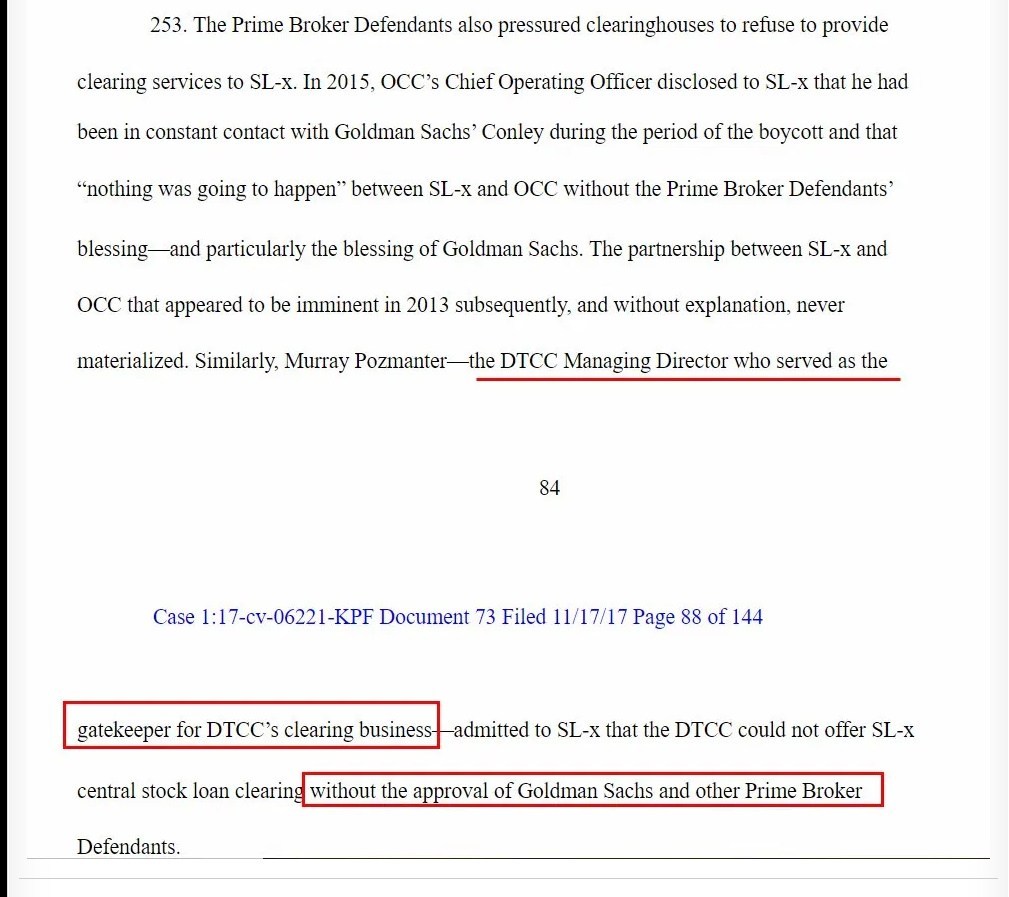

Sometimes they will count the votes on a “first-in” basis, and other times they will count the votes on a “last-in” basis, meaning your votes could be completely discounted in favor of somebody who borrowed stock immediately before the record date, or worse, they could include fake votes because one of their better customers had an interest in the outcome. Again, they own the DTCC, and Broadridge openly admits in their company SEC filings that their relationship with these brokers constitutes as a “Conflict of Interest”